This post may contain affiliate links which means that if you click through to a product or service and then buy it, I receive a small commission. There is no additional charge to you.

As a family, we always travel in my car. I love my trusty Honda CR-V. It’s got the kids car seats in, and is a family size car with plenty of boot space for all the million things which I carry around – just in case. We have a second car which my husband uses during the week for travelling to work. He has relatively low mileage on the clock as he primarily uses it to drive to and from the train station.

We are undoubtedly paying too much car insurance to be a two car household given the usage of the second car, but we don’t want to give up the flexibility of having two. Does this sound like you?

I’ve written this post in collaboration with By Miles, as I know that there are probably lots of households like us out there who are overpaying on car insurance for a car which isn’t being driven a lot.

By Miles offers pay-per-mile car insurance. They aim to offer competitive car insurance prices to those people driving less than 7,000 miles a year.

Want to find out if pay-by-mile car insurance could work for you?

If you know that you typically drive less than 7,000 miles a year, why not explore the option of paying less, especially as the quick quote tool from By Miles will give you an idea of what your price might be in under a minute (based on making a few assumptions).

If you like your quick quote price, and if you think pay-by-mile might be worth exploring further, just complete the rest of your details in the application to get a full quote.

Your full quote will be based on a range of questions about your car, personal details and driving history, and they’ll ask your estimated mileage for the year so they can give you an idea of how much it might cost you over the course of your policy.

How does By Miles work?

The By Miles concept is simple. By Miles thinks that the less you drive, the less likely you are to make a claim – it’s hard to have an accident when your car’s just parked outside your house.

On their a pay-by-mile car insurance policy, the less you drive, the less you pay.

By Miles splits the cost into two parts:

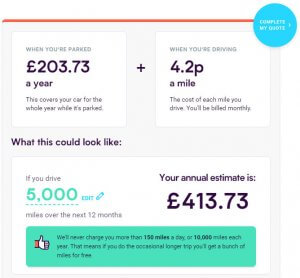

1) A fixed annual cost up front to cover your car while it’s parked. This is paid at the start of the policy.

2) You pay for the miles you drive each month.

So if you got the above quote and then drove exactly 5,000 miles over the year your car insurance would cost you £413.73.

The annual estimate of £413.73 is just the upfront fee of £203.73 and the total estimated mileage cost added together.

The estimated mileage cost = your estimated miles x your per-mile rate (5000 miles x 4.2p/mile = £210.00).

i.e. annual estimate = £203.73 + £210.00 = £413.73.

The estimate is just a guide. You only pay for the exact number of miles you drive each month.

No penalties for driving more (or less) than your estimate.

You need to have a rough idea of how many miles you drive each year to complete the quote. It’s like anything where you have to guesstimate whether how you behaved last year will be the same in the year ahead. We have to do it with everything from gas usage – who knows if it’s going to be a super cold winter that starts in October – through to car mileage; it can be hard to know! It’s tricky to predict your exact annual mileage when you just don’t know if you might change jobs, do a big driving holiday, need to use the second car more if something happens to your main car. The list goes on…

However, the good news is that a By Miles policy is pay-as-you-drive, so you just pay for the miles you drive (and not the miles you don’t).

To be clear, there’s no penalty for driving more or less than your estimate.

Can you drive as much or as little as you like. If you drive a little more than you guessed, you’ll pay a little more. If you drive less, you’ll pay less.

E.g. continuing with the above example:

a) If you drove less than your estimate (e.g. 4,500 miles), then over the year you’d pay the same upfront fee of £203.73 + (4,500 miles x 4.2p per mile) = £203.73 + £189.00 = £392.73.

b) If you drove more than your estimate (e.g. 5,300 miles), then over the year you’d pay the same upfront fee of £203.73 + (5,300 miles x 4.2p per mile) = £203.73 + £222.6 = £426.33.

c) If you didn’t end up driving at all (e.g. 0 miles), then over the year, you’d just pay the same upfront fee of £203.73 + (0 miles x 4.2p per mile) = £203.73 + £0 = £203.73.

By Miles – using technology to help customers.

- By Miles charges according to “how far you drive” and not on “how you drive” and your per-mile rate doesn’t change over the life of your policy. There’s no driver scoring and no penalties or price changes if you break or accelerate a bit too hard.

- They don’t report any speeding to the police (at least, not without a court order).

- There are no curfews.

- You don’t need an engineer to fit the Miles Tracker. Before you buy, they check your car’s compatible (most cars made in the EU after 2002 are). After you buy they send you a Miles Tracker in the post, it’s about the size of a small match box and you simply plug in yourself. If you have a problem just give them a call and they’ll talk you through it.

Lowering the cost of car insurance without compromising on quality

By Miles policies are fully comprehensive and come with:

- The flexibility of monthly payments with no added interest rate charges – most insurers charge you more if you opt for monthly rather than annual billing.

With By Miles, once you’ve paid your upfront fee for the year, you just pay for the miles you drive at the end of each month. That’s it. There are no interest rate charges.

This also helps you spread the cost of your insurance rather than paying it all at the start of your policy. - Capped mileage costs – you can drive as much or as little as you want. To help when you drive more:

- Daily mileage costs are capped at 150 miles, so the rest of your miles that day are free once you’ve driven more than 150 miles.

- Annual mileage costs are capped at 10,000 miles, so the rest of your miles are free once you’ve paid for 10,000 miles in a year.

E.g. if you go for a long drive of 250 miles in a day, then you remain fully covered but you are only charged for 150 miles for that day.

- No admin charges on your first 3 policy changes each year – most insurers charge you admin fees when you need to update your policy e.g. because you’ve moved house, changed car, added a person to the policy etc. By Miles don’t charge admin fees on your first 3 changes each policy year.

Note the price of your fixed annual cost and per-mile rate could still go up if e.g. if you move to a higher risk area or it could go down e.g. if you get a cheaper car.

Car insurance and then some

- No Claims Discount protection included as standard – even if you make a claim your No Claims Discount won’t go down

- Courtesy car while your car is being repaired

- 90 days fully comprehensive overseas cover (in any EU country)

- UK claims line

Also included as standard are: Uninsured driver cover (your NCD will be protected and you won’t pay an excess), Misfuelling cover, Replacement key cover, Personal belongings cover and Personal accident cover for the main driver and their spouse.

What’s the catch?

A By Miles policy won’t suit everyone. They currently only offer:

- Annual policies – there’s no option for short-term insurance/temporary cover

- Car insurance for people living in England, Scotland and Wales

Also:

- Policies are made for 25 to 76 year olds and so it’s difficult to get cover outside this age range

- If you end up driving more than you thought, you’ll end up paying more.

- They won’t be able to offer you insurance if they don’t think your car is compatible with their Miles Tracker (most cars are compatible).

- While they cover most people, there are a few other restrictions, these are mostly around people with higher risk profiles e.g. very expensive or high powered cars or people with many claims or convictions.

- Some insurance policies let you drive another car in an emergency. By Miles doesn’t include this. However if you are going to be borrowing someone else’s car, it might be worth making sure you have fully comprehensive cover rather than third party only cover, in case you crash it.

Find out if pay-per-mile could work for you

To find out more about By Miles and if pay-by-mile car insurance could work for you click here.