This post may contain affiliate links which means that if you click through to a product or service and then buy it, I receive a small commission. There is no additional charge to you.

I speak to a lot of people who say that budgeting just doesn’t work for them. They’ve tried and failed in the past to stick to a budget, and think they need a different way of managing their money.

If you’re serious about getting in control of your money and changing your behaviours, then you absolutely MUST master how to prepare a budget that works for you and which you can actually stick to.

I’ve collaborated with Emma, the money management app, in this article to talk about how to get in control of your money and crack the budgeting thing once and for all.

Anyone who has been following me for a while will know that I am not a big fan of the word ‘budget’.

‘Budget’ just screams restrictive and controlling. It’s like you are telling yourself what you can’t do with your money.

No-one wants to feel controlled by money; we just want to feel in control.

When I’m working with clients, we create a ‘spending plan’ instead. See, that sounds nicer already doesn’t it?

With a spending plan, the idea is that rather than cutting things out and restricting your spending, you give each pound you earn a job to do that is aligned to certain goals you have in mind.

It’s about being intentional with your money and where it flows to once it leaves your bank account!

How do I set a budget or spending plan?

You need to consider firstly how much is reasonable to put in your spending plan for each type of spending.

Bills, essential spending and necessities

To generate your monthly spending plan amounts for bills, essential spending and necessities, you’ll need to go through your previous spending history.

In the past, this would have involved printing out your bank statements and sitting down with a pen and probably a highlighter to sort through what you spent on what.

Luckily, technology is making this process easier for us.

Emma is a free app which I have been using for a while. You can link it up to as many of your bank accounts, credit cards, pension providers etc as you want, and it aggregates how much you have in each in an easy to use, visual dashboard.

Emma is super handy for getting a quick and easy overview of your finances as a whole.

It also features a great analytics tools. Your spending is analysed and split out by different categories (as well as by merchants if this information is useful to you). This gives you a huge head start when it comes to knowing where your money has gone in the past; which then helps you plan where it is going to go in the future.

You can also see easily see subscriptions and bills separated from standard spending which makes the task at hand much simpler.

For this part of the spending plan preparation, you need to be careful to make sure you have picked up all of your expenses, including any that are paid annually, and for which you might need to save in advance to be able to pay a one-off payment. I’ve listed some expenses below which can occur annually and which people frequently forget when they are putting together a budget or spending plan:

-

- Home insurance

- Car insurance

- TV licence

- Children’s birthday presents and parties

- Christmas gifts and parties

Sinking funds

Lack of detail is one of the main reasons budgets don’t work for most people. You need to ensure that you have planned for EVERYTHING which might require you to spend in any given time period.

Let’s do a bit of brainstorming…

- Start by listing all the goals you have and things you are going to need a pot of money to pay for. Don’t be tempted to stick with just the short term here; also consider things out to the medium and longer term. Here are some ideas to help you brainstorm:

-

- Building up an emergency fund

- Personal savings

- Holidays

- Large items

- Car maintenance or upgrade

- Home maintenance or extension

- Savings for children for their future

- Consider each goals and determine how much money you need for each.

- Look at how long it is until you need the money for that particular goal and work out how many monthly payments this equates to. Divide the total amount by the number of monthly payments required, to determine how much you need to save each month for that goal. Eg if you know you are wanting to go on an expensive holiday for a big birthday in 3 years, you would divide the total cost of the trip by 36 months to give you the amount you would need to save each month to reach your goal.

Here you’re creating what we call ‘sinking funds’ for future goals.

Without sinking funds, when the time comes that you need that money, if you haven’t planned for it and don’t have the money, you’ll end up either robbing from another part of your spending plan, or taking on debt to pay for it which we don’t want.

The order for your spending plan is important

Let’s keep this simple. Start with a blank sheet of paper with your income at the top. Then list the outflows for your spending plan in this order:

- Your personal savings sinking funds; this might include funds towards building up an emergency fund or your personal savings goals.

- Your essential spending eg rent/mortgage, utilities, council tax etc

- All the amounts for each of your sinking funds.

Take away all the expenses from your income.

If this calculation leaves you with a positive number, give the remaining money a specific ‘job’ – until you have a no more money to allocate. Be intentional about how you are going to use this money eg meal out with friends, or coffee once a week. Treats are fine – you are planning for them!

If you have a negative number, you’ll need to revisit your essential spending and sinking funds and re-prioritise. Can you find savings in your essential spending – look to compare your utility bills and see if you can get a better deal. With your goals, is there anything in there which you can postpone for a while until you have more disposable income?

Sticking with it

When we are starting something new, or which we know may be a challenge for us, having accountability is great.

In an age where our phones give us a huge amount of real-time information, it is great that they can be used to help us when it comes to accountability around budgeting.

With Emma, once you have the amounts which you are intending to spend on each category, you can plug these into the budget function on the app. Do double check that they add up to your total!

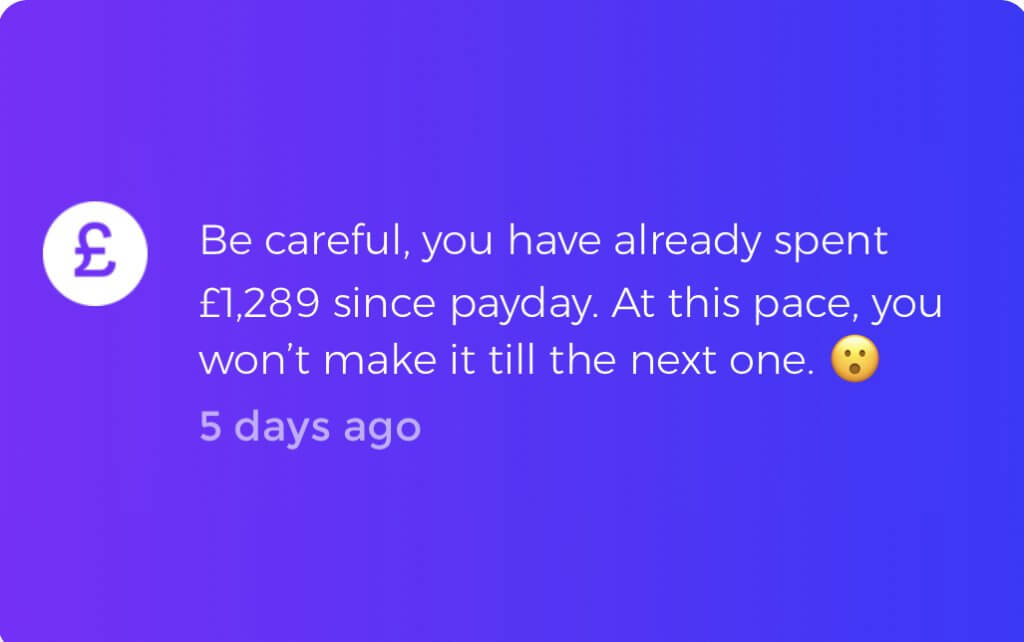

When you spend money via any of the accounts or credit cards linked to Emma on any category of expense, the available budget for that category will automatically be reduced. You’ll get a notification if you are looking like you are going to overspend on any category before the end of your budget period.

It’s so clever; it knows from analysing your bank statements when payday is so it can warn you that your rate of spending is too high to get you through until next pay day. (Artificial intelligence is very clever isn’t it – predicts our patterns of behaviour across the month. We are creatures of habit after all…)

Cool or what?

The importance of reviewing your spending plan

A spending plan is a fluid tool. Don’t think of it as something which is fixed once you set it up, and can’t be changed.

Reviewing it is crucial to your success in using it.

Stay on top of your essential spending and look for ways to reduce these bills.

You’ll want to review your sinking funds regularly; once you achieve a goal and don’t need to save for it anymore, redirect the money elsewhere. Be intentional all the time.

Make sure that you have enough flexibility within your spending plan. If you are finding that you haven’t allocated enough to a particular category, review the other categories to see where you might be able to squeeze some extra money for where it is needed.

Keep yourself accountable to sticking to it! Accountability is one of the best ways to ensure that you stick to a new habit or routine; Emma will help you with this with updates and prompts to bring your new spending patterns front of mind. The intention is to help you feel really in control of your finances.

If you are looking for more support around getting control of your spending habits and effective management of your behaviours around spending, come and join us in The Money Lounge, my low-cost monthly membership programme. Find out more here.