This post may contain affiliate links which means that if you click through to a product or service and then buy it, I receive a small commission. There is no additional charge to you.

As children grow up, there comes a point where you want to give them some financial independence. Are you wondering how best to allow your child the freedom to buy things themselves? How to monitor what they spend? And where they spend it? How to make sure it isn’t spent on things you don’t want them having money to buy?

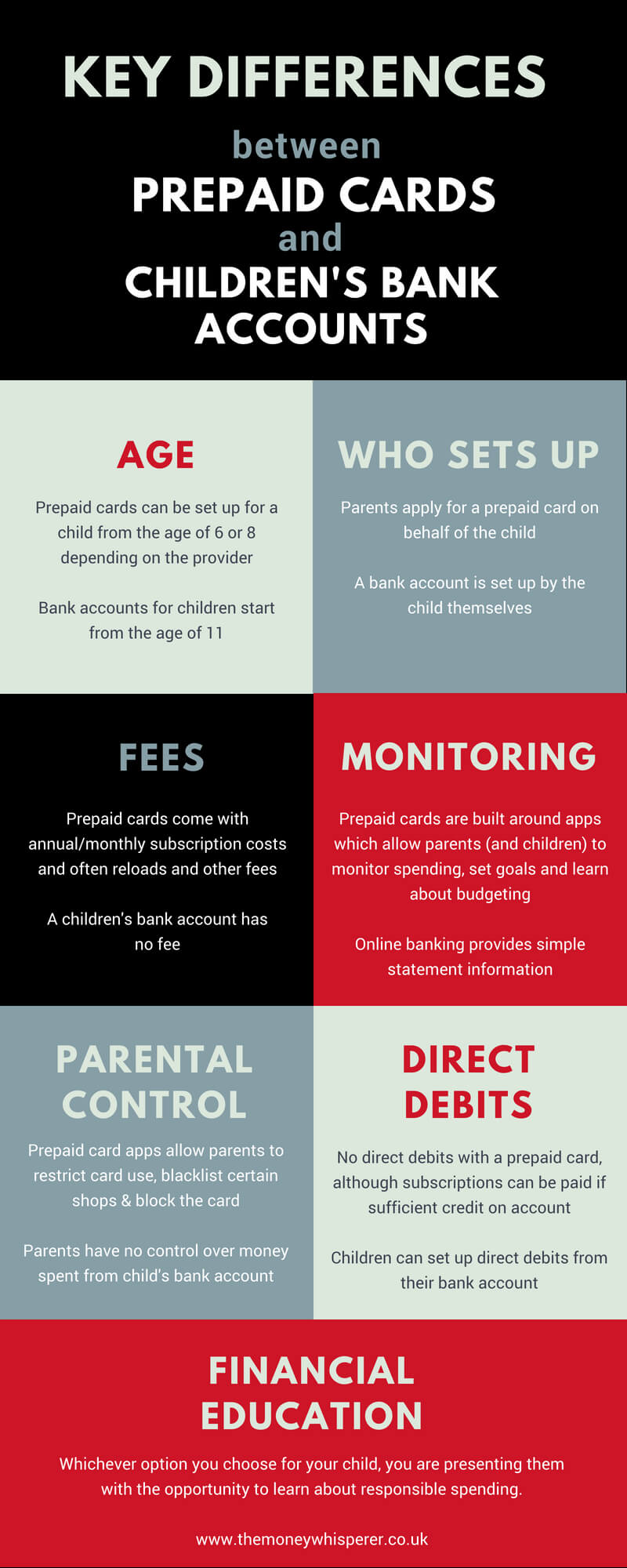

There are three main options available. Give them a cash allowance, opt for a prepaid card for children or a children’s bank account with card access.

Whether we like it or not, cash is no longer king. Children are growing up seeing adults using contactless cards and smartphone payment technology to make payments all around them. Whilst giving them pocket money in cash form is a great way to teach them to manage their money, I think it is important that older children are educated on how debit cards and current accounts work. This way, they can use them responsibly when they are adults.

But which is better and why? Here are the main differences between a prepaid debit card for kids and a children’s current account and associated card.

Prepaid card for children

There are several prepaid cards on the market, and a few of them are specifically for under 18s, including:

With a prepaid card, the parent loads money on to the card, which the child can then use just like a debit card. They can only spend up to the amount that has been pre-loaded and if there is no money on the card, they can not use it. It isn’t like a credit card and will not allow them to spend more than you have given them.

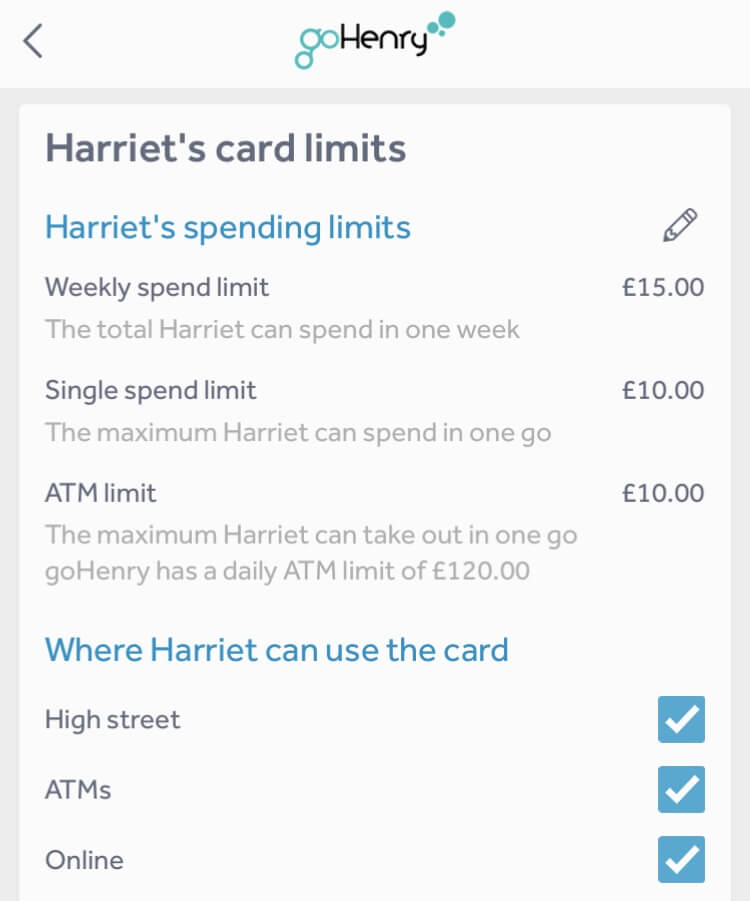

These accounts are built around apps which allow the parent to ‘control’ and oversee what their child is doing with their money. Parents can:

- Set maximum spending limits

- Review spending

- Receive text notification of spending including where they have shopped and what they spent

- Restrict card use at any of the following: ATM, online and in store (great if you want to prevent online misuse of the card)

- Blacklist certain shops and online sites

- Block the card if it is lost

This last feature is something that I love about my own app based banks. With a child, I can see that giving them a prepaid card for something like a school residential trip is far safer than giving them cash. If they lose the card, it can be blocked from the app.

This is what the parent monitoring screen of the goHenry app looks like.

Regular readers will know that I am usually a fan of a good app! In the same way that banking for adults is moving towards visual data rather than lines of text on a statement, the apps that sit behind these cards give more meaningful information too. The idea is that you can teach your children about budgeting in a user friendly way by allowing them the information to decide how best to spend it. They can see how much is left on the card in a way that you can’t with a traditional bank card.

Prepaid cards for children do attract a monthly fee which is a key difference to having a regular bank account. Whilst they are usually free to set up the account, they can have charges for:

- Monthly subscription to the service

- Personalised cards

- Loading on money – some include one parent load per calendar month as part of the service, others you pay for each load. Some charge for all methods of loading, others not if its via bank transfer etc.

- Replacement card if lost or stolen

- Using abroad

The charges for the cards below can be found by clicking on the links here:

All of the above prepaid cards offer a free trial period. You are not obliged to continue to use the card after the free trial– just remember to cancel your subscription or it will automatically charge you for the period after the subscription ends.

Children’s bank accounts

I have a vivid memory of the day that Midland Bank (now HSBC) came in to school and set us up with a bank account. We all got a navy blue binder with details of our brand new bank accounts, and our paying in books.

People are creatures of habit when it comes to their banks. I still have the same HSBC account today and whilst it isn’t my everyday current account, it’s the one account I know the sort code and account number for off by heart as I’ve had it for 30 years!

The great thing about a children’s bank account is that they have to open it themselves. The act of going to the bank and doing this (an adult will need to be present) can be a huge part of the financial independence learning experience for a child in itself.

Children’s bank accounts are essentially the same as adult bank accounts. The key reasons that we as adults choose to use a bank rather than a prepaid card as a home for our money are the same for a child:

- They are free.

- Trust in the big banks and their brand names.

- Money on deposit will earn interest. This is important as a means to teach children the value of delayed gratification – not spending the money the instant they have it will result in it earning interest.

- Direct debits and standing orders can be set up.

When a child opens a bank account, they will have the option to have a debit card, ‘cash card’ (or neither):

- With a debit card, the money can be spent anywhere and will be subject to a daily ATM withdrawal limit which the bank sets. There is nothing to stop a child withdrawing all of the money in their account (up to the daily limit of course). A parent can not place any restrictions on where the money is spent using the debit card.

- A ‘cash card’ will ONLY allow your child to withdraw money from ATMs; it can’t be used in store or online.

Some of the appealing features of prepaid cards which revolve around an app are not available with a bank account:

- Safety features are not inherent; if the card is lost, the bank needs to be contacted to block the card.

- There are no parental controls on where the child spends money.

- There are no limits on how much the child spends (short of restricting how much is actually in the account itself).

- There is no control over where the child spends the money.

For the best children’s bank accounts, take a look here.

My children aren’t quite old enough yet but when they are, I like the idea of the prepaid cards. I will have the visibility to monitor their spending. I also think the apps are great for helping teach wider financial concepts. When they have that grounding, I think they will be ready for children’s bank accounts at 11 years old. I think the lack of parental control associated with a bank account and debit card means I will want to know that they are relatively sensible with their money before I open one for them.

I’d love to hear your experiences of either a children’s bank account or prepaid card for children. If you have a child who isn’t old enough for a prepaid card or a bank account of their own yet, check out RoosterMoney, a great app for children to learn about money and money concepts through pocket money.

I’m taking part in the Monday Money linky with Lynn from Mrs Mummy Penny, Faith from Much More With Less and Emma from EmmaDrew.Info

I have the Go Henry account for my 8 year old son, however, we are not using it currently. Mainly as he can’t grasp the idea of pocket money yet. I will definitely give it another go soon though, as it looks perfect for parents.

Definitely take a look at RoosterMoney Clare as you can use token rather than money to understand goals and rewards etc

Being a very frugal person I dislike the idea of the monthly fee for these cards. However how they can be used and the lessons the young person can learn are far better than those gained from a bank account. If I had a younger child I think I would be swayed toward the pre-paid cards despite the fee.

Thanks for the detailed write up, I shall share with a friend who has younger children.

So far, I’ve stuck with giving my kids cash, and helping them open savings accounts with our local building society, so they can learn about putting money in and out and interest. Now my gaughter is older, I like the idea of pre-paid cards and more control via an app. Still a bit reluctant to pay a monthly fee though!

I hear you! The appeal of a fee free account definitely outweighs the benefits of the app functionality for a lot of my friends with old children in my unofficial poll…

I can’t believe how much choice there is compared to when I was growing up! Especially being able to choose what your children can use the card for – amazing!