This post may contain affiliate links which means that if you click through to a product or service and then buy it, I receive a small commission. There is no additional charge to you.

Child benefit and pension credits. Parents – particularly mums – are finding themselves at risk of losing thousands of pounds of retirement income because of an administrative bungle around the claiming of child benefit. It’s a topic close to my own heart as I am one of these mums myself.

Any person who cares for a child under 12 who isn’t in employment, and therefore isn’t receiving national insurance contributions, is eligible for national insurance credits.

But many simply aren’t getting them. I want to change that and have been campaigning with The Daily Mail over the last few months to get this issue addressed properly by HMRC.

The Department for Work and Pensions issued an alert last week aiming to encourage parents that ‘they may be inadvertently missing out on retirement income’. So many parents are missing out on these credits, and it needs a wider campaign to rectify the key causes.

I’ve been featured in The Daily Mail again this week urging the DWP to think about WHY people are missing out, and seek out a better way of managing the system.

There are two key reasons which affect the majority of those who are impacted.

If you fall in to either camp, please take action to register correctly as soon as possible to ensure you don’t miss out any more.

Not registered for child benefit

To receive these national insurance credits, you need to be registered for child benefit. However, not all families are eligible to receive child benefit; those earning over £50,000 get a reduced benefit and over £60,000 get none at all. These families frequently don’t sign up for child benefit. Why would you if you aren’t eligible to receive it?!

If you are a high-income family, ensure you still register for child benefit but tick the option to not receive it.

Working parent named to receive child benefit

Child benefit isn’t paid to a family, it is paid to a named individual. If you inadvertently put the working parent’s name on the child benefit form, they will also be the one who is eligible for the national insurance credits. However, if they are working they will be receiving national insurance contributions anyway so the credits are worthless to them.

If the working partner in your household is receiving the child benefit, it is possible to transfer credits to the non-working partner, if they are caring for a child under 12.

- For any year up to 5 April 2010, using form CF411.

- For years after 6 April 2010, you can only transfer credits for the most recent tax year, using form CF411A.

Why is this so important?

In order to receive the full state pension, you need 35 years of national insurance contributions and/or credits.

35 years is a substantial goal to achieve. Think about what age you started work and when you want to retire. Factor in periods of maternity or paternity leave where you weren’t working, any sabbaticals etc. For those parents who take extended time out of paid work while their children are little, these credits are often vital to meet that target.

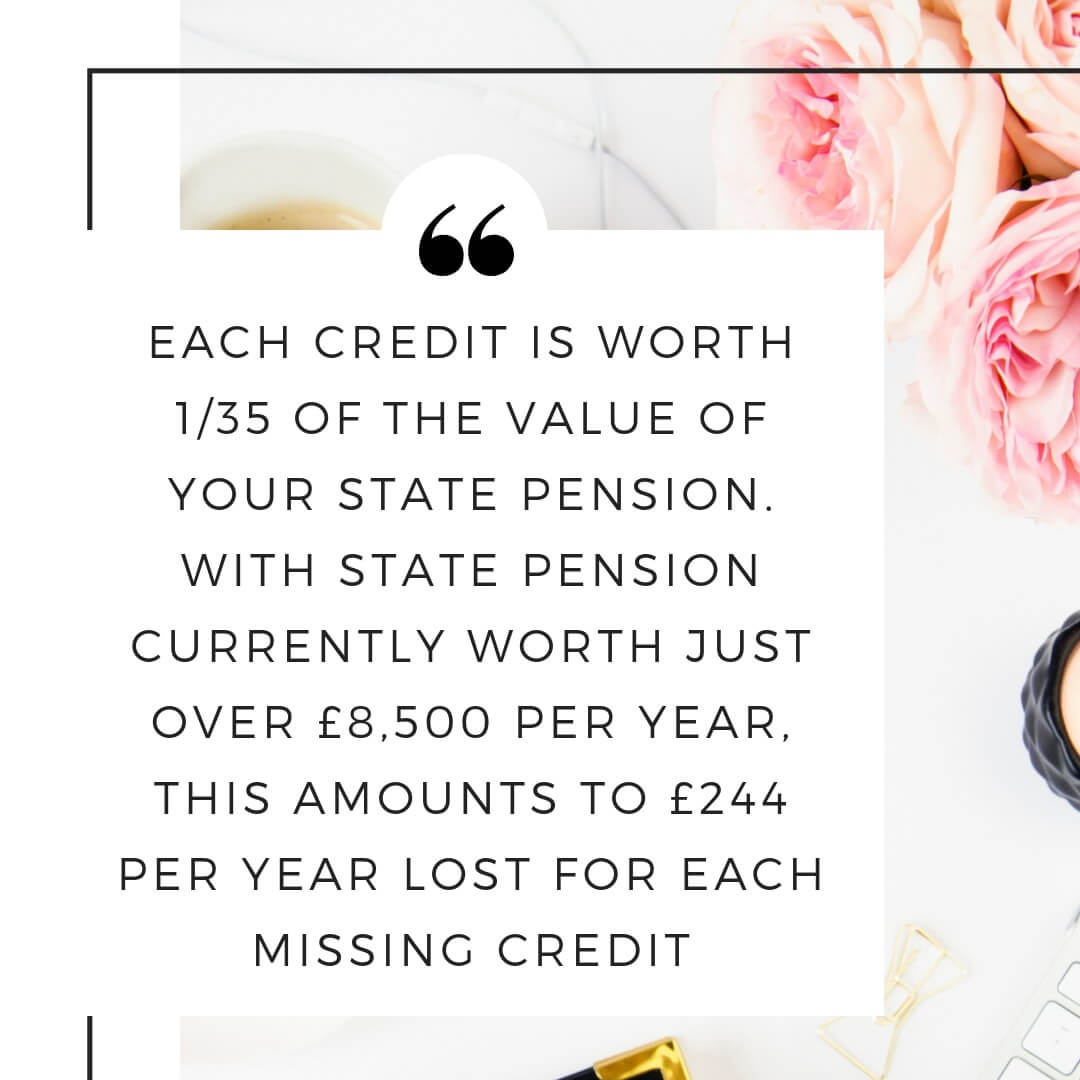

Each credit is worth 1/35 of the value of your state pension. With state pension currently worth just over £8,500 per year, this amounts to £244 per year lost for each missing credit. Say you live for 20 years after retirement, that’s almost £5000 you have missed out on for missing one credit.

I’m personally missing 4 years of national insurance credits for the years after my daughter was born. Unless I manage to hit 35 years of contributions from paid employment, those missing credits will leave me almost £20,000 worse off than if I had those 4 years of credits.

Useful to know….

- If you are belatedly registering for child benefit, you are only able to claim three months of back-dated credits.

- Grandparents who care for under 12s can also get credits, as long as they are of working age. Working parents can transfer unused credits to grandparents. Unlike with parents, a claim for transfer of credits to a grandparent can be backdated right the way back to 6 April 2011.

- You can complain to HMRC if you don’t understand why they have rejected a transfer claim.

- In the event you get an unsatisfactory answer from HMRC or your complaint remains unresolved, you can take your complaint to the Parliamentary Ombudsman. However, it must be referred by an MP so you will need to put your case to your local MP and ask that they put it forward on your behalf.

Personally, I would like to see the form changed to be a registration for national insurance credits (which are available to all), with an opt in for child benefit (which is not available to everyone). Alternatively, registration for national insurance credits could be linked directly to the registration of a child’s birth. The current opt in is leaving thousands of parents missing out which is ridiculous.

If you are affected by this, I’d love to hear from you. The campaign is looking for more case studies to take to HMRC to ask for a review of their situation.

A really helpful, and yet worrying article Emma!

Hello. I have literally just spent hours trawling the internet having heard an episode of Money Box about this recently . I had a child 6 years ago and did not claim as my husband is a high earner – like you – and will therefore have missed out on these payments in my state pension. I’m furious! I have had another child recently (last June) and am just getting around to the paper work so will have missed out further having not claimed within 3 months. Do you think it’s worth me writing a letter of complain when I submit my child benefit claim form? Thanks, Lucy

Hi Lucy, I have been working on the campaign with This is Money and Steve Webb since last summer but so far, the powers that be are adamant there will be no change to the backdating rules. There are thousands of us who this affects and it’s mainly women. It infuriates me as well! I don’t think a letter of complaint will make any difference unfortunately but please do get your child benefit form in as soon as possible.

Is there an easy way of checking if I completed a child benefit form for both of mine? Son is 5 next Jan and daughter is 3 in December? I was in employment until last September but took mat leave for periods, also recall completing the form for at least one of the children despite not claiming child benefit. I need to look into all of it. Thanks for alerting me to this. Doesn’t seem right.

Hi! You can check if you are receiving state pension credits by checking in your Government Gateway account.