This post may contain affiliate links which means that if you click through to a product or service and then buy it, I receive a small commission. There is no additional charge to you.

As with all investments capital is at risk and the value of investments and the income from them can go down as well as up and investors may not get back the amount originally invested.

Welcome to the second post in my mini series on retirement, which started last week with a post on how much should I be saving in to my pension.

Pensions are one of my core topics for 2019; the importance of having adequate savings for the future is something which I really want to hammer home to my readers.

As a nation, we simply aren’t saving enough for our future selves.

This week I have joined up with PensionBee, my own pension provider, to talk through the importance of appreciating the long term nature of pensions savings, and what that means for the choices which you make now.

Pension Age

In the UK, we don’t have a default retirement age. You get to choose when you want to retire.

I personally think that the traditional, rather black and white, periods of working then retirement, which characterised the lives of previous generations, will become increasingly more grey.

People are living longer, and spending a larger proportion of their adult life in retirement than in the past. When the State Pension was introduced in 1948, a 65-year-old could expect to spend 13.5 years in receipt of it – around 23% of their adult life. This has been increasing ever since. In 2017, a 65-year-old was expected to live for another 22.8 years, or 33.6% of their adult life.

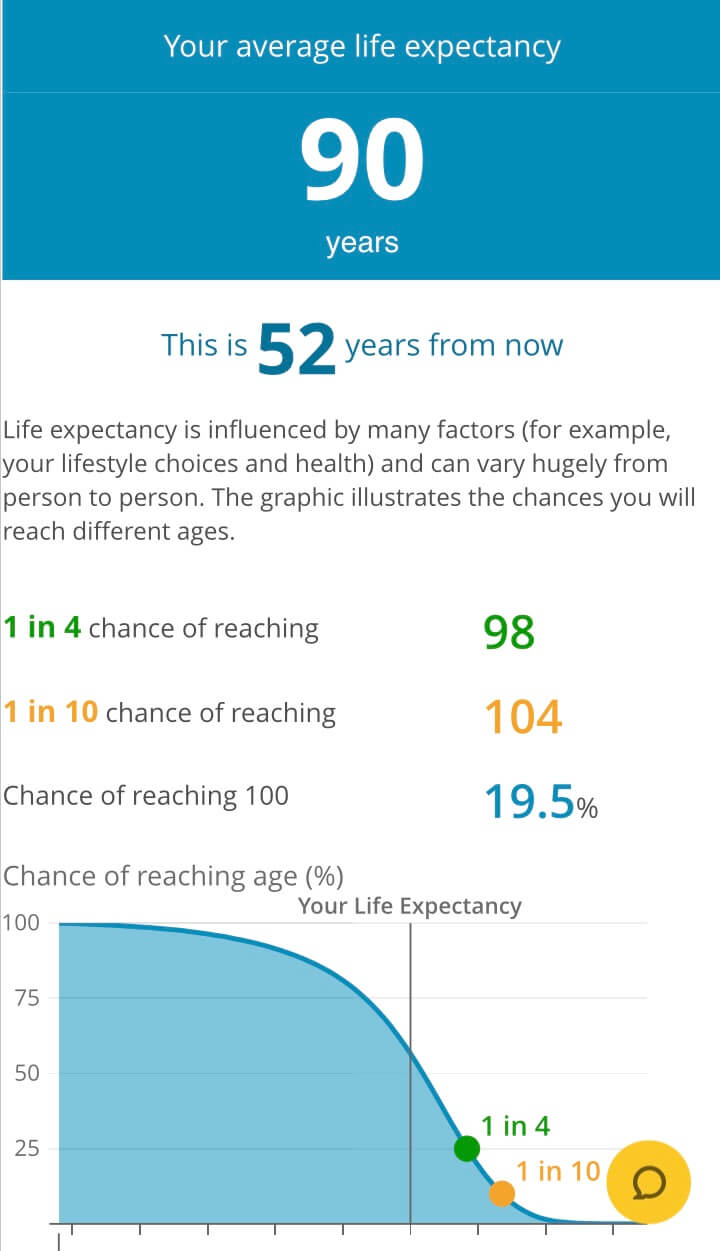

According to the Office of National Statistics, my life expectancy is 90, with a 19.5% chance of reaching 100.

If you want to see what your own life expectancy is based on your current age and sex, you can use the handy ONS tool on the PensionBee website here.

Those of us currently in our 30s who choose to retire in our 60s could feasibly need a pension to support us for 30+ years.

I think we will start to see a lot more people working for longer, maybe dropping down to a part-time capacity or deriving an income from an alternative source (I have a vision of YouTube granny influencers as I write this!).

Whenever or however you approach retirement, the absolute earliest that you can access any pension savings from either a defined benefit or defined contribution pension scheme is currently 55 (expected to rise to 57 in 2028).

The State Pension age is increasing for both men and women; currently 65, it’s rising to 66 by 2020 and is forecast to reach 67 by 2028.

The point here is that for the core demographic of my readers, retirement is a long way off.

The good news is that when it comes to growing the value of investments, time is our friend.Click To Tweet

It is hugely important to take advantage of the long time-frame over which you accumulate a pension. Here are 3 key things to consider:

Align your risk profile and your time to retirement

When you are investing your hard-earned money in any form of investment, your first reference point is your attitude to risk.

Whether you are risk tolerant or risk averse is affected significantly by the time you have until you want to access those investments.

In general, the shorter the time horizon until you retire, the less risk you will theoretically be willing to tolerate, as your priority is preserving the value of your pension investments. You don’t want them to suffer a large drop in value just before you need to drawdown your pension.

As retirement approaches, most people’s capacity for risk reduces year on year.

When you have a longer time horizon, short term volatility (ups and downs) in the stock market is less concerning as you have sufficient time for your investments to recover if there is a downturn in the market.

Monitoring your risk profile against your time to retirement is a hugely valuable exercise. If you have decades until you can access your pension, ask yourself if you are willing to accept a higher level of risk with the potential for a higher return on your investments. As the time to retirement approaches, most investors feel more comfortable moving a proportion of their investments in to less volatile, but lower return, products such as cash and bonds.

Don’t worry – you rarely need to think about doing all of this yourself. You just need to select a pension fund which has the right risk profile for you at the stage of life you are at.

Pension providers make your decision-making process fairly straightforward, providing access to a range of professionally-managed, diversified funds with different asset allocations (and therefore risk profiles).

The ‘Tailored’ plan I have chosen with PensionBee automatically invests my money differently as I move through life, moving my money in to safer investments as I get older. As I am in my 30s, my money is invested differently now to how it will be when I am in my late 50s. The younger I am, the more of my money will be invested in assets that are likely to grow, such as shares and property. This suits my risk profile well.

PensionBee has seven options to choose from, to suit different risk profiles and attitudes to investment, including an environmentally-friendly plan called Future World, a Shariah-compliant plan, and a couple of other newly launched plans geared towards protecting the savings of those nearing retirement.

Are you invested in your pension fund’s default plan?

Unless you are lucky enough to be in a final salary or defined benefit pension, what you end up with at retirement with depends on a combination of:

- How much you save plus any employer contributions, and tax relief

- How much your investments grow

Where your money is invested is crucial to how your investments grow.

If you have a personal pension, stakeholder pension or money in a workplace defined contribution scheme, you’ll commonly have to make a decision where your pension money is invested.

With the advent of auto-enrolment, millions of employees have been automatically enrolled into workplace pensions chosen by their employer. Typically, they may find themselves invested in a ‘default’ fund that is designed to suit as broad a range of people as possible.

Default funds tend to be cautious, lower-risk funds because of their one size fits all nature.

You want your investments to grow. You NEED your investments to grow. Remember the calculator which I talked about in this article, there is assumed level of growth applied to the money going in to your pension pot to help you achieve your desired monthly income in retirement.

Shares have historically performed better than cash or bonds over the longer term (although past performance is no guarantee of future performance). If you are invested in a fund which is heavily skewed towards lower-risk investments such as cash or bonds you will not see the same level of growth as a fund with a higher weighting towards equities (shares).

If you have a workplace pension, check if you have been automatically allocated the default fund. Have a read of the Key Fact Sheet for your fund which will provide you with the fund’s objectives, fees, asset allocation strategy and its risk profile (and how this may change over time). Compare this to other funds to see if you are invested in the right fund for your risk profile. It is advisable to seek the advice of a finance professional to talk through your choices. Your employer may provide this service to you.

Avoid short term, emotional thinking

When it comes to taking action, as humans, we can usually find an excuse not to do anything. I’m talking here to those of you who don’t have a pension at all. How many of you have ‘start a pension’ on your to-do list but it never gets actionned?

Humans also tend towards actions based on emotions. This is why you hear of people jumping on the bandwagon and buying shares at the top of the market, only for the market to pull back. And why you hear of people selling at the bottom of the market when they fear a further decline, only for the market to recover.

To achieve results, investing for the long-term needs to be void of any short-term, emotional reactions.

The markets have been a little up and down over the last few months. Then there is Brexit looming. There is so much we still aren’t sure about when it comes to the implications of Brexit, and we are now less than 30 days from D Day. However, this should NOT be an excuse to either delay your pension contributions, or <shudder> stop contributions all together.

Already we have seen a recovery from where they were at the end of 2018. There is no need to panic as a long-term saver. Short-term fluctuations are unlikely to cause any lasting damage, especially if you’re several years away from retiring.

Check out this great post on lessons we can learn from a recovering market.

History shows that whilst stocks markets swing up and down, the trend is always upwards. For this reason, times of volatility have often historically proven to be good times to invest.

Whilst a drop in the stock market might put you off adding an extra lump sum payment in to your pension, try and reframe your thinking. Instead of a risky time to invest, see it as a time to grab a bargain. When the market is down, funds are cheaper so you get more bang for your buck!

Don’t let your actions be driven by short-term, emotional thinking. The pensions game is a long one, where consistent action achieves results.

On a personal level, I have confidence that my pension at PensionBee is invested through the Tailored Plan in a mixture of stocks, shares, cash, property and even commodities. Investments are made in multiple locations around the world meaning that if any one market performs badly, there will be others in the mix with the potential to generate profits. The Tailored plan has performed really well against the FTSE 100 because of its diversification.

This is a collaborative article with PensionBee.