This post may contain affiliate links which means that if you click through to a product or service and then buy it, I receive a small commission. There is no additional charge to you.

As with all investments capital is at risk and the value of investments and the income from them can go down as well as up and investors may not get back the amount originally invested.

How much should I be saving in to my pension? This question is a bit of a ‘how long is a piece of string?’ type question because it depends on so many variables: when you started contributing and what the size of your pension pot is currently, how much you earn, how much you want to end up with when you reach retirement age, what age you think will start needing to draw on your pension and your other savings goals for the future.

Many people have lofty goals for how much they will have set aside in their pension pot, but they vastly underestimate how much they need to put away consistently to achieve that end result. Most retirees also hugely underestimate how long their retirement years will last, and therefore how much they need to support themselves.

So, what is a good pension amount? How much do you need to retire? And how much should you save in to a pension?

How much will I need in retirement?

The question of how much is a sufficient pension pot is a very important one. It’s the first step to determining what you need to save now – to ensure you get to that point in the future.

What you need to have saved ultimately depends on the standard of living which you want for your retirement. This will differ for everyone.

A general rule of thumb is that you will need an income in retirement which equates to 2/3 of your final salary to maintain the same standard of living.

This is based on the premise that your costs during retirement are typically a lot lower than during your working years. For many people, by the time they retire, they will have paid off their mortgage, their children will have left home and be supporting themselves, and their everyday costs reduce.

- If you don’t own your own home, you will need to factor in your continuing rental commitments throughout retirement, which will necessitate a higher retirement income.

- Don’t forget the State pension; the current full State pension works out at just over £8,000 per year. So, if you are targeting a retirement income of £30,000, you would need other pension income of c£22,000.

Experts say the average person needs a total pension pot worth £260,000 to enjoy a comfortable retirement. A pot this size would give an income of around £19,000 a year, including the state pension.

This is not a small figure!

By the time we want to stop working, we’ll be mortgage-free, the girls will have been through university, and our costs will be lower than now as most of what we do currently revolves around entertaining and feeding our little family. We may not need two cars if there is no longer any commuting for either of us. Our holidays will be cheaper as there will only be two of us to pay for!

In our future plans, we know that we want to do a lot of travelling when the girls have left home. We need enough saved to visit everywhere on our bucket list. This means that in addition to pension savings, we are acting now to ensure we have income coming in even when we have stopped working – through property, other investments and alternative income streams.

If you are like us and will have other sources of income when you retire, this reduces your reliance on your pension income. Maybe this is something you want to explore alongside thinking about your pension savings?

Have a think about what you want out of retirement and what retirement income you will need to sustain this lifestyle.

It’s an interesting exercise to look at your current monthly outgoings and think about what these will look like for you when you are in your 60s (or whenever you plan to retire). Strike through anything which you will no longer need to pay for e.g mortgage, or which will reduce significantly e.g. commuting. Factor in any new costs such as travel plans or new hobbies (flying planes can be expensive!).

This should give you a good idea of the level of income you need to support yourselves through retirement.

Reverse engineer your goal

Once you know how much income you need in retirement, you can reverse engineer that goal to understand how much you should be saving now in order to get there.

What actually gets invested in to your pension is a combination of:

- Your contribution

- Your employer’s contribution

- Tax relief

Plus, remember you will likely also receive the state pension. (Those of you who are familiar with me will know that I am not 100% convinced of this for those of us with a fair few years until state retirement age!)

Check out my post here on ensuring you are registered correctly for child benefit so that you will receive state pension credits

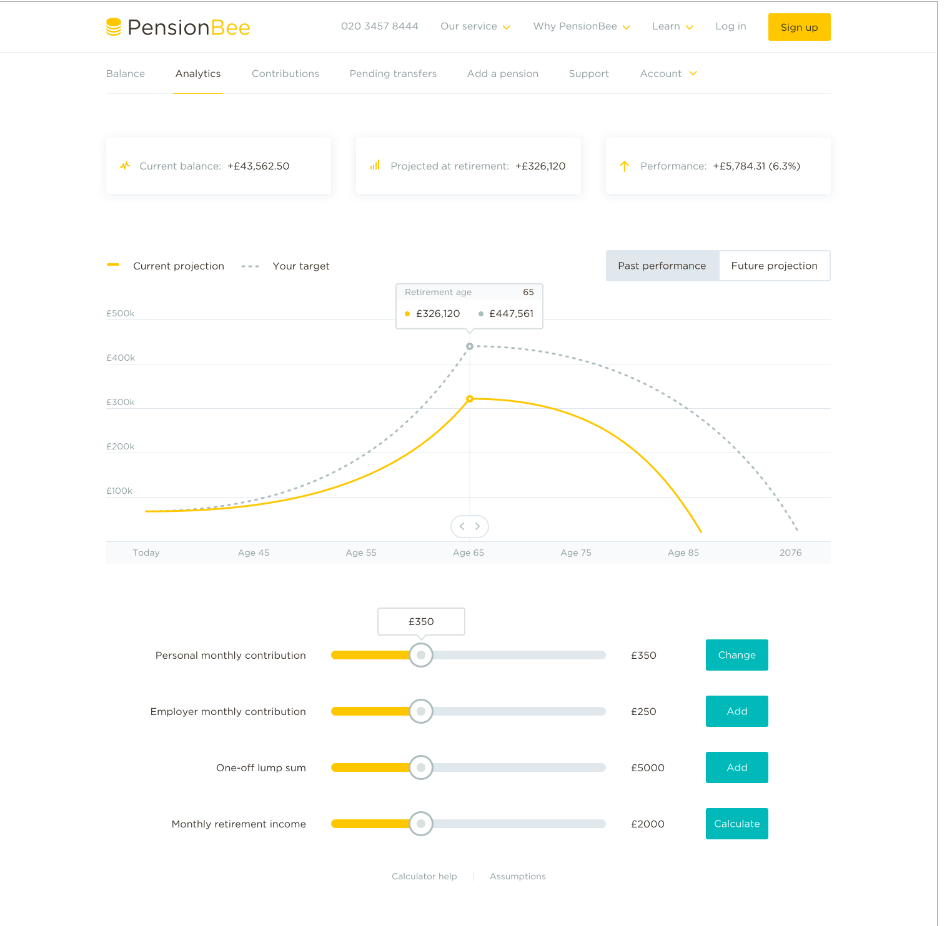

PensionBee have a great pension calculator which enables you to set your retirement income goal, and see if your current contributions are going to get you there.

You input your current age, your current pension pot and then you can play around with your future contributions, and those of your employer until you find the level of contributions you need to achieve your projected retirement pot.

It’s so simple to use; the sliders help you get a sense of what you should be saving to reach your desired outcome, in just a couple of clicks.

Have a play with the calculator. It certainly made me consider the power of increasing my monthly contributions. Adjusting the inputs using the sliders allows you to decide how much you need to save to help you reach the retirement income goal you set. Alternatively, it may be a reality check, helping you to understand that you may need to delay your retirement if your current contributions aren’t going to get you to your income goal.

Do remember, a calculator is just a tool and it can only make estimates: the value of your investments can go up as well as down, and there are lots of factors that could affect the value of your pension pot at retirement.

Start saving as soon as possible – the power of compound interest

Although retirement may seem a long time away, and there will always be competing priorities for our money, the earlier you start to put aside money in to a pension, the better off you will be.

The money you invest in the early days will be invested for the longest time and has the best chance to grow through the power of compound interest.

Check out this great video which explains the power of compound interest and how it acts like a snowball rolling down a hill to grow your pension pot.

I’ve contributed to a book which is being launched on International Women’s Day next month; it’s aimed at teaching life lessons to teenage girls. One of the things I talk about is the importance of getting in to the saving habit. Starting to contribute to a pension gets you in to a positive savings habit, and you never miss that money if you start right from your very first pay packet.

If there is one thing which I wish someone had explained to me better when I was younger, it was the power of pensions savings. I remember getting pension forms when I started my first job and they had lots of jargon in them which I didn’t understand. They are not generally known for being hugely user-friendly, are they? The forms were confusing and I wasn’t really sure whether it was a good idea to lock money away forever (that’s what 55 seemed like to me when I was 22!)

The later you start your pension, the more you will need to contribute to accumulate the same size pension pot. As a rule of thumb, you need to contribute half of your age in pre-tax salary – if you are 40, you should think about contributing 20% of your pre-tax salary in to your pension.

Even if it feels that you can’t afford pension contributions at the moment, or you have more immediate financial goals – maybe you are saving for a house deposit or building a fund to send your children to university – every little helps.

Try and get in to the habit of contributing little and often even if you are on a tight budget, and benefit from the power of compound interest.

This is a collaboration with PensionBee.

I need to check the details of mine. I know I contribute to it each month and so does my employer but I’m not sure how much or what it’s currently worth!

I have one with my employer but no idea how much I’ll get. I need to look in to this